Turning Up the Heat on BREIT | April 2025

On the two-year anniversary of one our most read REIT outlooks, ‘Arbitrage Opportunity Available in Public REITs’, we will be revisiting some of the predictions and observations on non-traded REITs versus public REITs from April 2023. To summarize the April 2023 REIT Outlook, we warned investors that the ‘mark to magic’ (what we call the flawed valuation process for non-traded REITs) Net Asset Values (NAVs) needed to be revised downward to reflect the negative impact of higher interest rates, while public REIT valuations were already reflecting lower pricing (higher yields) and had less than half of the debt leverage relative to their non-traded counterparts.

One of the drivers of the flawed ‘mark to magic’ process is the ‘appraisal lag’ that is based on recent transactions that have been negotiated many months, or even quarters, prior to NAV valuation date. This lag persists to this day despite the signals provided by public REITs.

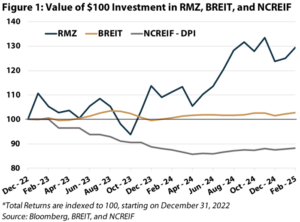

As shown in Figure 1, from March 31, 2023 to December 31, 2024, the MSCI US REIT Index (Bloomberg: RMZ) produced a total return of +20.4% while the NCREIF National Property Index (NCREIF NPI), an index that tracks values of private real estate, produced a total return of -5.8%. An index that tracks the daily NAVs of non-traded REITs (NCREIF Daily Priced Index, or DPI) produced a total return of -9.4%. Improbably, BREIT, the largest such non-traded REIT, produced a total return of +2.0%.

BREIT’s performance is obviously surprising in what was a very tough environment for commercial real estate. In our opinion, it reflects a need for further downward revisions. In fact, the April 2023 outlook suggested a ‘public market’ price for BREIT that would have been 60-70% lower than where it was trading at the time. We believe this is still true today.

With BREIT’s recent positive performance, it now boasts a +106% cumulative total return through December 2024 since its January 2017 launch. Given the significantly higher contributions in 2020-2022, we calculate the average BREIT investor has received a cumulative total return of +30%, assuming a June 30 investment date each year from 2017-2023. However, if BREIT’s NAV were to be calculated using public REIT implied pricing metrics as of December 31, 2024, the average BREIT investor would have lost over 3%.

We applaud any investors (and especially readers!) that were able to redeem out of non-traded REITs and re-invest into public REITs. While our call proved correct for the past two years, we believe there is still more to come. Banks have been willing to work with real estate owners to extend maturities in hopes of lower rates in later years, and cap rates have been relatively steady (though still higher than where many ‘mark to magic’ cap rates were at the time), which has minimized markdowns to non-traded REIT NAVs. However, recession fears are bubbling up again, and expectations for several future Fed Funds Rate cuts have been taken off the table. Therefore, we are re-iterating our call for future outperformance by public REITs versus non-traded REITs for the next two years.

What We Got Right (and Wrong)

In 2023, the market was worried about a recession as a result of the unprecedented swiftness of the Federal Open Market Committee’s (the ‘Fed’) decision to raise the Fed Funds Rate from 0-0.25% in March 2022 to 4.50-4.75% in March 2023. The 10-year Treasury yield had risen from 2.6% to 3.6% in the prior year, and public REITs were coming off of their second-worst year of all time, producing a -24.5% total return in 2022, as measured by the RMZ.

In comparison, non-traded REIT net asset values (or NAVs) had yet to reflect the declines in the public REIT market. In fact, several non-traded REITs, including BREIT, were still marking up NAVs. In our view, the higher leverage consisting of primarily variable rate debt, conflicts of interest, high fees, and the need to sell properties to meet redemptions would necessitate downward revisions to non-traded REIT NAVs. In contrast, public REIT valuations already reflected a higher interest rate environment and had bullet-proof balance sheets ready to pounce on distress, leading to a scenario where public REITs should outperform non-traded REITs significantly.

While we were correct, the aforementioned 2,000-3,000 basis points (bps) of outperformance has not yet brought public REIT and non-traded REIT valuations in-line with each other. To be clear, there are several non-traded REITs that were forced into bankruptcy and investors were left holding the bag. However, the largest non-traded REITs are still alive and kicking…for now.

There are several reasons they have been able to avoid a reckoning. First, the economy did not go into a recession. Job growth continued, and GDP proved resilient in the face of rising rates. Despite two more rate hikes in 2023 and a 10-year Treasury yield that eventually peaked at 4.9% in October 2023, consumers spent and businesses thrived, as evidenced by 2023-2024 posting the first back-to-back years of over 20% total returns for the S&P 500 since 1997-1998.

Second, banks’ non-real estate loans were in very good shape as a result of the strong economy, and thus were able to work with over-leveraged real estate owners to implement remedies such as extending maturities. Furthermore, to the extent banks did require an equity infusion to right-size loan-to-value ratios (as a result of a declining value), many owners have been able to source equity from new investors to plug the gap.

Third, capitalization rates (or ‘cap rates’, calculated as net operating income divided by property value) in the private market have been steady for most property types. While the transaction market fell off of a cliff in 2023 declining 54% from the prior year according to Green Street Advisors, transactions increased by 22% in 2024, giving investors more data points to conclude that cap rates had not increased as much as the 10-year Treasury yield. Notably, we had used a 6.5% cap rate for rental housing in our BREIT NAV estimate, in-line with public residential REIT pricing at the time, much higher than the low 4% implied by BREIT’s NAV. As of December 31, 2024, CBRE’s multifamily cap rate survey indicated cap rates were approximately 5.1%, and, recently, there have been multiple large REIT-quality transactions at cap rates below 5%. This is surprising given the further ~100 bps increase in the 10-year Treasury yield to 4.6% on December 31, 2024, indicating investors are: 1) hoping to refinance at lower rates in the future, 2) expecting significant increases in net operating income, 3) hoping that lower rates bring down cap rates further, or 4) willing to accept lower returns.

In summary, other than the increases in borrowing costs, things could not have gone any better for non-traded REITs in the past two years versus what could have been expected in April 2023, allowing many to maintain elevated NAVs with aggressive cap rates. Even those faced with redemptions that could have triggered property sales at valuations below NAV found a way to survive using one of their preferred tools: the redemption gate.

Hate the Gate?

The most difficult part of capitalizing on the arbitrage between non-traded and public REITs in April 2023 was the inability to redeem out of several non-traded REITs. In the April 2023 Outlook, we noted that BREIT had reached its stated limit for redemptions for the prior five months, only fulfilling 5% of equity value per quarter. This continued until February 2024 when BREIT was finally able to meet 100% of redemptions for the first time since October 2022.

S-REIT, a large non-traded REIT sponsored by Starwood, has gone the other way, unfortunately for investors. Due mostly to balance sheet mismanagement and the aforementioned weak transaction market, S-REIT actually reduced the maximum redemption from 5% per quarter to 0.33% per month in May 2024. As of March 31, 2025, S-REIT has limited investor redemptions for 29 straight months.

UC Investments Update

As readers may recall, one source of BREIT’s enhanced liquidity was a $4.5 billion investment from UC Investments at extremely favorable terms (to UC Investments). To secure this cash infusion, Blackstone agreed to provide up to $1.125 billion in BREIT shares (derived from performance fees Blackstone had paid itself) to make up the difference between actual performance and an 11.25% annualized net total return hurdle rate for UC Investments from December 2022 to December 2028. As of February 2025, UC Investments’ annualized total return on its BREIT investment is +1.3%. To reach the 11.25% hurdle, BREIT will need to produce a cumulative total return of +84% from March 2025 to December 2028, or +17.3% annualized. For reference, BREIT has only had one year (2021) where its total return was more than +12.3%.

BREIT NAV Refresh

Simply taking the 2024 fourth quarter’s annualized net operating income and dividing into the December 2024 NAV results in an implied cap rate of 4.3% for BREIT (keeping constant BREIT’s estimated fair value for unconsolidated investments). Using the same method for December 2022, the NAV two years ago implied a cap rate of 4.4%. As such, despite BREIT speaking about higher discount rates and exit cap rates in its 2024 year-end stockholder letter, we believe that the valuation remains aggressive, especially compared to the public REIT implied cap rate of 5.9% as of December 31, 2024. To get more granular, the weighted average implied cap rate of public industrial and rental housing REITs, which comprise 85% of BREIT’s consolidated gross asset value, was approximately 5.4% as of the same date, still a 20% difference.

Therefore, using the blended REIT implied cap rates for BREIT’s consolidated portfolio, we estimate a ‘comparable NAV’ of $9.17 per share, which is 33% lower than BREIT’s December 31, 2024 stated NAV per share of $13.71 for the I-shares.

To repeat the exercise of where BREIT would trade in the public market, we can update leverage, payout ratio, and general and administrative (G&A) costs as a percent of gross assets.

As of December 31, 2024, BREIT’s consolidated leverage stood at approximately 60% based on historical cost, a slight decline from the 64% we calculated for December 31, 2022. We note that BREIT does not report debt on its unconsolidated investments, which would push the ratio higher. Similar to 2022, BREIT has significant exposure to variable rate debt, much of which has been hedged with interest rate swaps and caps. Of the fund’s $60 billion in property and unsecured debt, approximately $39.9 billion (or 67%) is variable rate debt. However, BREIT states that its actual variable rate exposure is only 12% due to its swaps and caps. We cannot determine the costs paid for these swaps and caps, but it is fair to assume that all of these were not costless.

Furthermore, BREIT has a staggering $33 billion in debt coming due by the end of 2027. Given poor disclosure practices, it is not possible to determine the interest rate on expiring debt, but the weighted average fixed rate on its fixed mortgage debt is 3.8%, well below where current refinancing rates are today. Adding credence to the future refinancing headwinds for BREIT, the fund has $26 billion in swaps maturing by the end of 2027 with a weighted average SOFR/EURIBOR strike rate of 1.4%. In comparison, the SOFR and EURIBOR rates as of March 31, 2025 were 4.3% and 2.4%, respectively. Assuming a 200 bps higher interest rate on refinancing $33 billion in debt, BREIT’s AFFO minus management fees would decline by $660 million pushing it well into negative territory, all else equal. For reference, BREIT’s AFFO minus management fees was $501 million in 2024. In comparison, as of December 31, 2024, the weighted average leverage ratio of public REITs was 31%, fixed rate debt was 92%, and the weighted average maturity of debt was 6.4 years.

Management fees and G&A costs for BREIT in 2024 totaled $778 million, which equates to 0.9% of gross consolidated real estate. This is a drop from 2022 due to a lack of performance fees paid by shareholders to Blackstone, which was also the case in 2023. In 2022, performance fees were $743 million, which pushed the G&A ratio to 1.1%. In comparison, the average public REIT G&A ratio was 0.5% as of December 31, 2024.

Finally, BREIT continues to pay a dividend above and beyond its cash flow. In 2022, we calculated a dividend payout on adjusted funds from operations (or AFFO) minus management fees of over 270%. We subtract management fees from BREIT’s AFFO because BREIT is externally advised and pays fees to its adviser using shares of its common stock. BREIT paid dividends in 2022 of $0.71 per share for the I-shares, which compares to $0.68 per share in 2024, a 4% decrease. However, AFFO minus management fees went from $0.25 per share in 2022 to $0.13 per share in 2024, a 47% decline. As a result, we calculate the payout ratio in 2024 was a whopping 519%! In comparison, public REITs increased dividends by approximately +2% from 2022 to 2024, and AFFO increased by 6%, resulting in a dividend payout ratio as of December 31, 2024 of 74%.

Onward and Upward for Some, Onward and Downward for Others

In the April 2023 outlook, we noted that the above-mentioned leverage, G&A, and dividend payout attributes are so far off the scale for how we value public REITs, it is difficult to determine where BREIT would trade, but we estimated it would be 60-70% below its stated NAV. Despite the lower cap rates implied by comparable public REITs, we believe that a similar discount would still be applied today. However, with the company’s ability to put up a redemption gate to prevent forced sales, the catalyst for reaching our estimate remains unknown.

Shareholders that decide to stay invested should be concerned about their dividend. We note that the 40% drop in AFFO minus management fees per share in 2024 coincided with a healthy +4% same store net operating income (NOI) growth. We believe same store NOI growth will be lower in 2025 than 2024 for BREIT based on public REIT guidance (unfortunately missing from BREIT’s disclosures). Combined with the aforementioned refinancing headwinds, it is difficult to project any growth in AFFO minus management fees for the near term. As such, if BREIT were public, we would advise management to cut the dividend to 80% of AFFO, or $0.10 per share, which would be 85% lower than today’s payout. Even at $0.10 per share, the dividend could be at risk without significant same store NOI increases or declines in the 10-year US Treasury yield over the next two years. Notably, public REITs would also benefit greatly in such an environment.

In contrast, we project public REITs will grow AFFO by ~3% in 2025, which will accelerate to 5-6% in 2026 and 2027. With their fortress balance sheets, we believe public REITs could further enhance this growth by 50-100 bps per year through accretive acquisitions. As a result of this growth and the low payout ratio, public REIT dividend growth should be in the +5% range annually for the foreseeable future.

Combining the 4% dividend yield as of March 31, 2025 for public REITs and a 5% growth rate, we believe public REITs could produce an annualized total return in the 9-10% range, which we believe will comfortably outpace BREIT.

Matthew R. Werner, CFA

mwerner@chiltoncapital.com

(713) 243- 3234

Bruce G. Garrison, CFA

bgarrison@chiltoncapital.com

(713) 243-3233

Isaac A. Shrand, CFA

ishrand@chiltoncapital.com

(713) 243-3219

Thomas P. Murphy, CFA

tmurphy@chiltoncapital.com

(713) 243-3211

RMS: 2,998 (3.31.2025) vs. 2,966 (12.31.2024) vs. 3,177 (12.31.2021) vs. 1,433 (3.23.2020)

An investment cannot be made directly in an index. The funds consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.)

The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security. Past performance does not guarantee future results.

Information contained herein is derived from and based upon data licensed from one or more unaffiliated third parties, such as Bloomberg L.P. The data contained herein is not guaranteed as to its accuracy or completeness and no warranties are made with respect to results obtained from its use. While every effort is made to provide reports free from errors, they are derived from data received from one or more third parties and, as a result, complete accuracy cannot be guaranteed.

Index and ETF performances [MSCI and VNQ and FNER and LBUSTRUU] are presented as a benchmark for reference only and does not imply any portfolio will achieve similar returns, volatility or any characteristics similar to any actual portfolio. The composition of a benchmark index may not reflect the manner in which any is constructed in relation to expected or achieved returns, investment holdings, sectors, correlations, concentrations or tracking error targets, all of which are subject to change over time.

Leave a Reply

for more info on our strategy

go now →

for more info on our strategy

go now →

VIEW CHILTON'S LATEST

Media Features

go now →

Contact Us

READ THE LATEST

REIT Outlook

go now →