The Cost of Staying Public in a Discounted REIT Market | April 2026

In the early 1990s, the Modern REIT Era commenced due to the abundance of overleveraged private real estate companies with no path to new equity other than to ‘sell’ shares to the public at a price below their perceived value. To quote Chilton REIT Strategy founder Bruce Garrison, “they had to decide whether they wanted to own 100% of something worth zero, or a lower percentage of something with actual value.” Over the next 30 years, public REITs proved that the public path was an avenue to create wealth for shareholders, as well as founders and management teams, compounding total returns at +7.9% from 1992-2021 using the FTSE NAREIT All Equity REITs Index (Bloomberg: FNER).

However, selling 100% of a company is a different decision that mixes personal incentives with business incentives. A whole company sale usually results in job losses, sometimes for those making the decision to sell (or not). Therein lies the ‘principal-agent problem’ of investing.

We believe that the public REIT market is ripe for mergers and acquisitions (M&A), and have thought so for several years. While 2026 is off to a good start due to a $10.7 billion public-to-public merger of National Storage Affiliates (NYSE: NSA) into Public Storage (NYSE: PSA) and a take-private of Veris Residential (NYSE: VRE) for $3.4 billion, we are optimistic that more REIT management teams and boards of directors will put personal considerations aside and act in shareholders’ best interests in 2026.

NAV: Irrelevant Until It’s Not

Net Asset Value, or NAV, is the estimated private market value of a company. All else equal, in an efficient market, public REITs would have market prices that reflect current NAV plus or minus the public’s perception of future NAV growth.

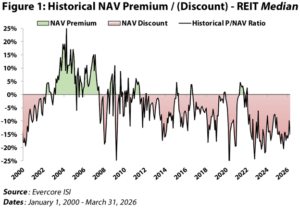

However, as of March 31, 2026, the median REIT trades at a 15% discount to NAV (Figure 1), and the 86 public REITs we cover range from a 55% discount to an 87% premium. In fact, public REITs have traded at a discount on roughly 88% of trading days in the past 16 years! Why is that? How could management teams sleep at night in this environment? Why haven’t they been active in selling their companies? Why haven’t buyers stepped in to buy them on sale?

The Persistent NAV Discount

Fortunately, or unfortunately, the market price is determined precisely by the meeting point at which buyers are willing to pay and where sellers are willing to sell. More sellers than buyers result in price declines as they race to unload shares, and vice versa. Several factors help explain the persistent discount over the past 10 years.

First, the proliferation of passive funds (or ETFs) has contributed to more indiscriminate buying and selling, which, at the margin, have been able to diminish the influence of active managers that are carefully analyzing the underlying companies. In the past, a good company at an NAV discount with the potential to grow NAV per share would attract disproportionate interest from REIT-dedicated buyers to close the gap. ETFs, on the other hand, buy and sell based on the underlying index allocation and flows in and out of the ETF, regardless of NAV discount.

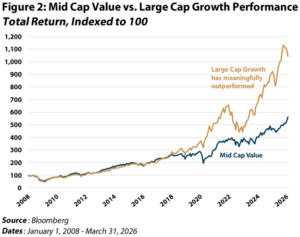

Second, generalist investors (non-REIT-dedicated investors) place less emphasis on NAV. The outperformance of growth vs value stocks over the past 10 years is clear evidence of limited generalist interest in the value proposition of REITs, regardless of the discount. Furthermore, the median equity market capitalization of public REITs was $2.7 billion as of February 28, 2026. This firmly puts the average REIT in the ‘mid-cap’ classification, another area that has underperformed over the past decade (Figure 2). In fact, according to the March 2026 Bank of America Investor Survey, real estate remains the most heavily underweighted sector by generalist investors at 16% below their respective benchmark weights.

Third, the rise of non-traded REITs (NTRs) from the ashes, as well as the growth of real estate private equity, diverted flows that would have otherwise gone to public REITs. We have discussed this at length in previous publications, but the main contributors to this trend were: 1) low interest rates, 2) a cost-of-capital advantage from higher leverage, 3) fees paid to brokers by NTRs for allocations, and 4) perceived low volatility.

Follow the Capital Allocation Tree

Essentially, a REIT at a steep discount and elevated leverage is stuck in a ‘capital box’ whereby it cannot raise new equity or debt to pursue external growth. According to our capital allocation tree, discussed here, the correct capital allocation move in this case is to sell assets and buy back stock. The next decision if stock buybacks are not effective would be to sell the company. So why has this not been happening?

The Principal-Agent Problem

The principal-agent problem is the conflict of interest between a manager (e.g. CEO, Board of Directors) and an owner (e.g. shareholders). An example of this in everyday life is the conflict between a homeowner and a real estate agent. While a homeowner would like to get the highest price, an agent is incentivized to get a deal done, with price as a secondary consideration.

REIT CEOs enjoy an annual compensation package that is difficult to walk away from. The Board of Directors is tasked to devise compensation plans that align CEO interests with shareholders, but this is an imperfect solution with inherent conflicts. In theory, shareholders can exert influence through proxy voting on compensation plans and board nominees, but the cards can be stacked in favor of the desires of management.

In fact, some public REITs have structural features that limit shareholder influence: 1) domiciled in Maryland, a state viewed as less shareholder-friendly, 2) the use of MUTA (Maryland Unsolicited Takeover Act), which allows a company to adopt anti-takeover defenses without shareholder approval, 3) an ownership limit of 9.9% without a waiver from the board of directors, and 4) high passive ownership, which means convincing proxy advisor services such as ISS and Glass Lewis can make or break any proposal.

As such, activism, an investing style that publicly pushes for changes or a sale through proxy voting, has historically been lower for REITs than in other sectors. This has further contributed to persistent NAV discounts by diminishing one of the main tools that shareholders can use. In spite of these roadblocks, activism in REITs still exists and is increasing.

‘Tis the Season

We believe that REITs should be attractive to generalist and activist investors today due to: 1) discounts to NAV, 2) increasing NAVs, 3) expectations for further rate-cuts by the Federal Reserve, 4) low obsolescence risk, and 5) rising replacement costs. With so many positive attributes, any REIT that is not trading close to NAV should take a hard look in the mirror and ask whether continuing on the current path is best for shareholders.

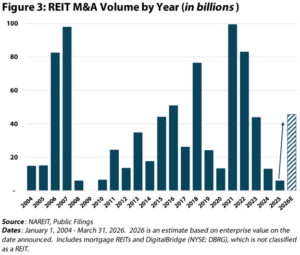

Based on announced deals through March 31, 2026, we are on track to double the total REIT M&A from the past two years combined, as shown in Figure 3. In addition, this total should grow over the next 9 months as we are tracking more REIT activism today than we can remember.

Based on deals announced in the past year, the average transaction has resulted in roughly a 20% to 40% premium to the unaffected share price. And, while most of the CEOs and board members likely lost their jobs after transacting, they potentially gained a reputation for shareholder-friendly decisions, which can promote future opportunities.

We have two companies in the Chilton REIT Composite that are ‘in play’ as of March 31, 2026: Centerspace (NYSE: CSR) and Whitestone (NYSE: WSR).

Centerspace

We have been following CSR for many years, including a headquarters visit and property tours in Minneapolis. The company draws its history back to an IPO in 1997 when it was called Investor’s Real Estate Trust and owned a diversified portfolio across residential, medical office, retail, industrial, and senior housing. In 2017, the company changed its name to Centerspace and began a painful journey (for earnings per share) to 100% multifamily properties in the Midwest. As of December 31, 2025, CSR owned 12,000 units, with Minneapolis and Denver as its top markets.

Anne Olson was appointed CEO in 2023 and pursued a strategy to close the gap to NAV, albeit in a difficult environment. The company sold properties in tertiary markets, expanded into new markets such as Salt Lake City, and used a redevelopment program to boost cash flow at existing properties. Due to high leverage, the company was not able to buyback a meaningful amount of shares. None of the strategies ultimately attracted enough investor attention to close the gap, and, on November 11, 2025, CSR announced that the company was pursuing strategic alternatives.

We immediately engaged with management and initiated a position based on our belief that the company could close the gap between market price and NAV through a sale of the company. As of March 31, 2026, CSR is trading at an estimated 7.1% cap rate, which compares to an estimated private market cap rate of 5.9%, resulting in a 30% discount to NAV. While a transaction is not guaranteed, we are confident that this management team will make the best decision available for shareholders, whether it is a full company sale or a steady liquidation. Notably, multifamily peers Veris Residential and Elme Communities (NYSE: ELME) are in the process of liquidation and have outperformed the average multifamily REIT by 3,160 and 3,430 basis points, respectively, since announcing those plans.

Whitestone

Our history with WSR goes back more than a decade. Headquartered in Houston, and with over 20% of its net operating income coming from the market, we have a deep understanding of the unique property set. We have also toured most assets in the Phoenix and Dallas markets (40% and 20% of the portfolio, respectively). The company has traded at a meaningful discount to NAV for most of its history since its 2010 IPO due to high leverage, high general and administrative costs (G&A), a high dividend payout ratio (over 100%), and corporate governance concerns.

In 2022, the company fired the CEO for cause, cut the dividend, and began a path toward lower leverage. As of December 31, 2025, leverage had declined to 7.0x net debt/EBITDA (from >9.0x in 2019), the payout ratio was 70%, and G&A as a percentage of assets had declined to 1.5% (from nearly 2% in 2019). However, corporate governance concerns are re-entering the story after rebuffing takeout offers for the company in 2024 and 2025.

We began buying WSR in June 2025 at an average price of ~$12.35 per share, with the view that the company’s NAV per share would be growing due to strong performance of retail assets (a large overweight in the Chilton REIT Composite), and the potential for a take-out at a price close to NAV. Already, the former CEO has proposed a new slate of directors for the upcoming annual meeting, and there are rumors of other shareholders pursuing proxy campaigns. We sent a letter to the Board of Directors in November stating that the company was vulnerable to activism unless they decide to pursue strategic alternatives to close the NAV discount.

On March 5, Reuters reported that WSR had hired Bank of America to advise the company on a sale process, and TPG and Blackstone (NYSE: BX) had expressed interest in making offers. This follows increasing activity from Blackstone in the shopping center space: ROIC ($4 billion) closed in February 2025, ALEX ($2.3 billion) closed in March 2026, and a $440 million Texas portfolio purchased early this year.

As of March 31, WSR trades at a 7.6% implied cap rate, which compares to an estimated private market cap rate of 6.8%, resulting in a 15% discount to NAV. We would also argue that the private market cap rates for open air retail are trending lower, meaning a buyer could potentially pay a premium to current NAV.

Conclusion

While we are hopeful that CSR and WSR will make the best decisions for shareholders, we can’t be sure. History is littered with failed takeovers and activism attempts, especially in REITland. Elliott, a leading activist investor, was successful in gaining board seats at Rexford (NYSE: REXR) and Crown Castle (NYSE: CCI), and the share prices of these companies are ~18% and ~22% below their levels when the positions were publicly disclosed, respectively (unaffected share price based on REXR’s closing value on August 26, 2025, and CCI’s closing value on November 24, 2023).

However, the mere threat of activism is welcome in 2026 for active REIT managers such as ourselves. We strongly believe that any public REIT with a market capitalization below $5 billion and trading at an NAV discount of 15% or more should seriously consider strategic options; failure to do may result in attracting activists that can leave reputational scars, successful transaction or not!

Matthew R. Werner, CFA

mwerner@chiltoncapital.com

(713) 243-3234

Bruce G. Garrison, CFA

bgarrison@chiltoncapital.com

(713) 243-3233

Thomas P. Murphy, CFA

tmurphy@chiltoncapital.com

(713) 243-3211

Isaac A. Shrand, CFA

ishrand@chiltoncapital.com

(713) 243-3219

RMS: 3,201 (3.31.2026) vs. 3,054 (12.31.2025) vs. 3,177 (12.31.2021) vs. 1,433 (3.23.2020)

An investment cannot be made directly in an index. The funds consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.

The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward-looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security. Past performance does not guarantee future results.

Information contained herein is derived from and based upon data licensed from one or more unaffiliated third parties, such as Bloomberg L.P. The data contained herein is not guaranteed as to its accuracy or completeness and no warranties are made with respect to results obtained from its use. While every effort is made to provide reports free from errors, they are derived from data received from one or more third parties and, as a result, complete accuracy cannot be guaranteed.

Index and ETF performances [MSCI and VNQ and FNER and LBUSTRUU] are presented as a benchmark for reference only and does not imply any portfolio will achieve similar returns, volatility or any characteristics similar to any actual portfolio. The composition of a benchmark index may not reflect the manner in which any is constructed in relation to expected or achieved returns, investment holdings, sectors, correlations, concentrations or tracking error targets, all of which are subject to change over time.

Leave a Reply

for more info on our strategy

go now →

for more info on our strategy

go now →

VIEW CHILTON'S LATEST

Media Features

go now →

Contact Us

READ THE LATEST

REIT Outlook

go now →