REIT Roadmap for Generalist Investors | October 2016

September marked a watershed moment in the REIT historical timeline: the creation of its own top-level GICS sector, appropriately named ‘Real Estate’. We addressed the potential long term impact of this change in our May 2016 REIT Outlook, in particular as it relates to the sector’s raised profile and new capital flows that may boost valuations. However, indiscriminate REIT buying and/or incomplete due diligence could produce results below generalist expectations, further delaying a full embrace of the new sector. REIT analysis requires some unique steps to properly determine the relative ‘attractiveness’ of one REIT versus another, including the understanding that traditional equity analysis techniques may actually prove counter-productive.

Though the dividend yield is a portion of the total return (less than half), much more exhaustive research needs to be done to assess the potential price changes and risks. Our methodology is based on the premise that, using a company’s comprehensive disclosures and transparency of comparable property transactions, we can accurately determine the intrinsic value of a REIT and properly adjust for the risk of achieving this value.

Generalist vs Dedicated

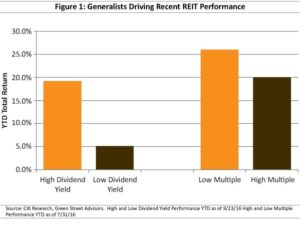

From our conversations with REITs and Wall Street analysts, generalists seem to differ from REIT-dedicated investors in their attraction to high dividend yield and low multiple REITs, which we believe is evidenced by the outperformance of high dividend and low multiple REITs recently, as shown in Figure 1. While multiples and dividend yield are part of the due diligence process, there are many other factors to consider. We believe we can provide some additional data points for generalists to consider before jumping on the REITrain.

While a generalist is benchmarked to a broad equity index containing REITs such as the S&P 500, REIT-dedicated investors benchmark to a REIT-only index. Benchmarked to the MSCI US REIT Index, the Chilton REIT Team focuses only on investing in US REITs and real estate related companies. Because our universe is more concentrated, we have the opportunity to be more exhaustive in our research. In contrast, generalists may ignore (and many have) REITs for the simple reason that other sectors in their benchmark screen more attractive and they presumably do not understand the unique vocabulary and valuation metrics associated with real estate.

The reality is that assessing the attractiveness of REITs does not work when applying traditional equity screens, especially those related to GAAP (Generally Accepted Accounting Principles) terms such as net income, book value, and earnings multiples. In contrast, we look at NAV (Net Asset Value), FFO (Funds from Operations), AFFO (Adjusted Funds from Operations), and subjective items such as quality to determine risk and potential returns. Furthermore, generalists should be aware that comparisons across geographic regions and property types may prove difficult.

Be Wary of ‘Cheap’ Stocks

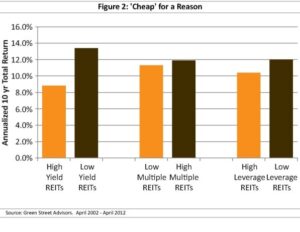

High dividend yields and low multiples can be quite misleading. While some investors may be attracted to a higher dividend yield due to the quicker return of cash to shareholders, often it is indicative of higher risk than REITs with low dividend yields. Similarly, REITs with low AFFO multiples may seem ‘cheap’, but often are cheap for a reason. In fact, using data from Green Street Advisors shown in Figure 2, REITs with low dividend yields outperformed REITs with high dividend yields, and REITs with high AFFO multiples outperformed REITs with low AFFO multiples in the 10 year period ending April 30, 2012, representative of a full real estate cycle. While we certainly would not say that these rules work 100% of the time, it’s a lesson that more research needs to be done.

Yield Comes with a Cost

The first risk to assess is leverage. Higher leverage equates to higher risk, which in turn should equate to a higher expected return in order to compensate investors for the risk. However, as shown in Figure 2, REITs with low leverage outperformed REITs with high leverage over a full cycle.

To analyze leverage, we use some broadly-known ratios, including net debt to EBITDA, interest coverage, and net debt to total enterprise value. Debt to equity, a widely used ratio outside of REITs, is not useful given that REIT book value of equity is depressed due to high depreciation expense and often dividend payouts in excess of income, both of which lower retained earnings. Instead, we look at debt to gross asset value (book value of real estate plus accumulated depreciation) or debt to an estimate of the market value of assets based upon our internal financial models. As of August 31, 2016, the REIT average net debt to EBITDA was 6.0x and the average debt to gross asset ratio was 33%.

The composition of a REIT’s liabilities is also important. Debt maturities should be laddered such that no single year has an inordinate amount of debt due. Similarly, a longer weighted average maturity of debt equates to lower risk. The weighted average maturity of REIT debt is approximately 5.4 years. Additionally, we encourage companies to use preferred equity as a source of funds, as it does not need to be paid back. Assuming a 50 year maturity for preferred equity, merely adding a 10% sleeve to the liability stack increases the weighted average maturity to over 10 years. In general, we prefer that debt be unsecured so that a REIT has the option to increase secured debt if the capital markets close. Due to the uncertainty of floating rate debt, we prefer companies that use mostly fixed rate debt. The weighted average REIT exposure to floating rate debt (excluding debt swapped to fixed) was 19% as of June 30, 2016.

All Dividend Yields are Not Created Equal

Another risk to consider is the payout ratio. A company may have a higher yield merely because it is paying out a higher percentage of cash flow. Unlike common stocks, equity REIT dividend payout ratios are typically based on AFFO instead of GAAP net income. FFO and AFFO, which add back depreciation and other non-cash charges from net income, measure REIT cash flow more accurately than net income (which includes non-cash charges).

Similar to Free Cash Flow (or FCF), AFFO represents the cash generated by the company after any reinvestment necessary to maintain the portfolio (also called maintenance capital expenditures). One of the oddities of GAAP accounting is that real estate companies are allowed to capitalize many costs associated with maintaining real estate which we believe should be expensed as they occur. As such, AFFO is the most conservative measure of REIT cash flow available for either reinvestment or paying dividends to shareholders.

A lower dividend payout ratio creates greater optionality for capital allocation, and therefore lowers the need to access the capital markets to pursue growth opportunities. In addition, a lower dividend payout ratio provides higher security that the current dividend will not be cut, as well as a higher probability that it will increase in the future. As of August 31, 2016, the weighted average REIT payout ratio was 74% of AFFO.

Yield as a Valuation Tool

Understanding that generalists will always be interested in the dividend yield of REITs, it can be used to assess the ‘cheapness’ of the sector relative to historical averages. The most popular tool is to measure the spread between the dividend yield and the risk free rate, represented by the US 10 year treasury yield. Historically, the spread between the REIT dividend yield and the US 10 year treasury yield has averaged about 110 basis points. While those attempting to compare current AFFO multiples to historical averages or compare REIT AFFO multiples to non-REIT FCF multiples may conclude that REITs are expensive, the dividend yield spread is sending a much different signal.

As of September 30, 2016, the spread was 234 basis points (or bps), implying that REIT dividend yields need to compress 124 bps to return to the historical average, or that the 10 year US treasury yield is going to rise by 124 bps in the near future. To return to the historical average dividend yield spread, REIT prices would have to increase by approximately 46%. We don’t see that happening immediately, but if the 10 year US treasury yield does not rise as much as the market implies, we believe there would be upward pressure on REIT prices.

Growth > Yield

REITs with high yields or low multiples also may be priced as such due to a slower growth profile. Our methodology treats returns from appreciation with the same weight as returns from yield, and therefore we are interested in the drivers of appreciation such as earnings growth (which actually translates to dividend growth) and NAV growth. Historically, growth has been a better predictor of future returns than dividend yield.

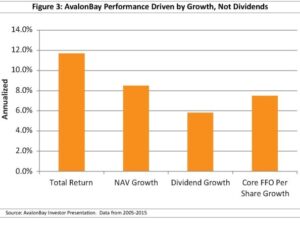

Instead of merely participating in changes in rents and values over full cycles, REITs can dramatically increase earnings and NAV through development. Apartment REIT Equity Residential (NYSE: EQR) created over $1.8 billion in value creation due to development from 2005 to 2015. Apartment peer AvalonBay (NYSE: AVB) had similar success over the same period, generating annual NAV per share growth of 8.5% (see Figure 3), which comprised 73% of the total return to shareholders.

In addition, NAV per share is a much more useful valuation tool than earnings multiples. In its simplest form, NAV is calculated by dividing annual net operating income (or NOI) by a capitalization rate (or cap rate, equivalent to NOI/Market Value) to determine the market value of real estate assets. Company-specific cap rates can be built by using a weighted average cap rate for the properties in the portfolio using comparable transactions and third party estimates. After deducting liabilities and preferred stock, and dividing by the number of shares outstanding, the NAV per share is compared to the market price per share, resulting in either an NAV premium or discount.

In general, a REIT that is trading at a discount to NAV would be considered ‘cheaper’ than one trading at a premium. It doesn’t mean that the stock will outperform, as there could be reasons for the discount in one stock versus another. However, it’s entirely possible for a stock to trade at a discount to NAV, but also trade at a high AFFO multiple, thus sending a misleading signal to any investors looking only at AFFO multiples. We use a proprietary system that assesses balance sheet risk, management competency, and efficiency to determine the proper premium or discount to NAV at which a stock should trade, which we believe can more accurately identify ‘cheap’ REITs relative to the value an investor will receive over a holding period.

More Than a Yield Vehicle

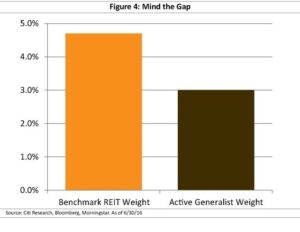

REITs have a huge opportunity to gain a new investor base. The opportunity is apparent from generalist investors who remain approximately 40% under-invested in REITs relative to their benchmarks as of June 30, 2016, as shown in Figure 4. We hope that the GICS change will illuminate the fact that REITs are more than a collection of income-producing assets that provide a dividend yield. These are living, breathing companies with a long history of value creation.

Since 1992, about two thirds of the total return of the NAREIT All Equity REIT Index (Bloomberg: FNER) has come via the dividend. However, in the past 10 years, dividends have accounted for less than half of the total return, partly due to the compression in cap rates for commercial real estate. We believe that anyone looking at this newly minted top line GICS sector as merely a yield vehicle could be misled by any number of preconceived criteria. Instead, we encourage spending a little more time to at least identify the historical drivers of outperformance, and thus how to put together the portfolio with the best risk-adjusted returns going forward.

Parker Rhea, prhea@chiltonreit.com, (713) 243-3211

Matthew R. Werner, CFA, mwerner@chiltonreit.com, (713) 243-3234

Bruce G. Garrison, CFA, bgarrison@chiltonreit.com, (713) 243-3233

Blane T. Cheatham, bcheatham@chiltonreit.com, (713) 243-3266

RMS: 1904 (1.31.2017) vs. 1904 (12.31.2016) vs. 346 (3.6.2009) and 1330 (2.7.2007)

Previous editions of the Chilton Capital REIT Outlook are available at www.chiltonreit.com/reit-outlook.html.

An investment cannot be made directly in an index. The funds consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.

The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security.

for more info on our strategy

go now →

for more info on our strategy

go now →

VIEW CHILTON'S LATEST

Media Features

go now →

Contact Us

READ THE LATEST

REIT Outlook

go now →