The Trump Effect on Equity REITs | December 2016

Since our previous publication on November 1, 2016, there have been quite a few changes in the economic and political outlook for the US. Surprisingly, the election results boosted equity markets to all time highs, despite pundits who suggested beforehand that a Republican sweep would be negative for the market. The main reason for their skepticism was the uncertainty that surrounds the President-elect, which contrasted to the continuity promised by the Democrat candidate. Somehow, this uncertainty has allowed market participants to find potential positives of the regime change for seemingly all parts of the economy. By no means do we believe we have a better crystal ball than others on what Donald Trump and a Republican Congress could do to change the equity REIT environment. However, we can present how certain stocks have reacted thus far and assess the outcomes of potential new policies.

The Broad REIT Market

In November, the MSCI US REIT Index (Bloomberg: RMZ) produced a total return of -1.7%, which compared to the S&P 500 (Bloomberg: SPX) at +3.7%. The pullback was driven by massive net outflows from REIT ETFs and mutual funds, totaling $1.3 billion in the three weeks for which we have data in November. Prior to the election, REIT ETFs and mutual funds had experienced net inflows of $21.6 billion for 2016. We assume that the reason for the allocation shift away from REITs was due to higher interest rates, reflected in the increase in the US 10 year treasury yield from 1.83% on October 31 to 2.37% at the end of the month.

We try to always highlight the growth profile of our holdings, and that REITs should be viewed as total return stocks. Higher interest rates as a result of an increase in inflation and economic growth expectations will ultimately drive higher growth in rental income at the property level given an equilibrium between supply and demand. However, even using metrics that are commonly used for yield investments, REITs are already discounting a further rise in interest rates.

With the REIT Index yield at 4.17% versus the US 10 year treasury yield of 2.37%, the spread between the two was 180 basis points (or bps) as of November 30. In comparison, the historical average spread is 110 bps, thus sending a strong ‘cheap’ signal to yield investors. In fact, assuming the dividend yield spread returns to the historical average, REITs would produce a positive two year total return even if the US 10 year treasury yield rises to 3.6% by the end of 2018! For reference, the yield curve as of November 30 implies a 10 year yield of 2.8% at the end of 2018.

Apartments

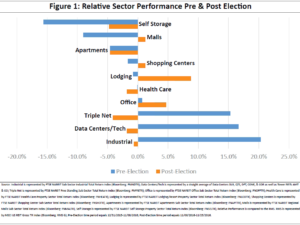

The FTSE NAREIT Apartment Index (Bloomberg: FNAPT) underperformed the MSCI US REIT Index by 460 bps year-to-date through November 8 as shown in Figure 1, driven mostly by fears of oversupply in core markets such as New York City, San Francisco, Washington, D.C., and Seattle, which comprise 25% of the sector’s Net Operating Income (NOI). Without commensurate job and wage growth, the market is assuming that REITs will have a difficult time pushing rental rates due to the increased competition from new construction.

Since the election, apartments underperformed the index by 510 bps. The underperformance may be attributed to some negative comments at an industry conference during the month and comments made by Trump about Government Sponsored Enterprises (or GSE’s; ie. Fannie Mae), but we believe that investors should focus more on the effects of higher job and wage growth, deregulation, and defense budget increases.

In particular, any volatility in the financing environment due to GSE reform would have a disproportionately negative effect on private developers and owners. Public REITs are funded mostly through unsecured debt, so this would actually give them a cost of capital advantage over their private counterparts. It would likely lower new construction, which would help to assuage fears of new supply reaccelerating after 2017.

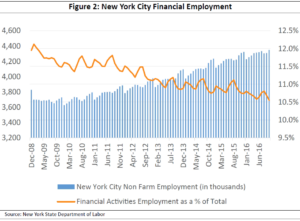

New York City has been the poster child of the decline in the Financial sector since the Great Financial Crisis. In addition to lower profits due to the downturn, restrictions and regulations significantly impacted the ability for these companies to rehire personnel. From December 2007 to January 2010, the city lost 210,000 jobs, of which about 50,000 were in the ‘Financial Activities’ sector. Despite adding back 723,000 jobs from January 2010 to October 2016, only 38,000 finance jobs have been added over the same period. As shown in Figure 2, Financial Activities jobs as a percent of total NYC jobs has declined by over 150 bps since 2009 as a result. President-elect Trump has explicitly stated his intent to lower regulations on banks, particularly repealing some or all of Dodd-Frank. If this is proposed and passed through Congress, it could lead to higher profitability for the banks and more hiring within the city. This scenario would help to alleviate the perceived supply problem that is not expected to be at an equilibrium until 2018.

The outlook for the Washington, D.C. apartment market is also more optimistic. Since 2001, the DC market experienced 36.5 msf of office absorption in the 6 years that the Presidency and Congress were aligned, while the market lost 6.5 msf of occupancy when the two branches were divided, per JLL Research. 2017 will be the first time since 2009-2011 that the legislative and executive branches will be aligned, which bodes well not only for office absorption, but also for apartments within the region. Donald Trump also is planning to ask Congress to reverse defense budget cuts from the 2013 sequester and rebuild the military.

Since 2010, defense spending has dropped by 15%, negatively impacting defense-related employment in the D.C region as the area typically receives (and thus loses) more than 20 cents of every procurement dollar spent (or not spent). However, defense spending is set to slowly increase through 2017 due to the Bipartisan Budget Act of 2015. If Trump follows through with some of his comments, the increased spending should contribute disproportionately to apartment fundamentals in the region.

Shopping Centers and Regional Malls

The Shopping Center and Regional Mall sectors, represented by the FTSE NAREIT Shopping Center Index (Bloomberg: FNSHO) and FTSE NAREIT Regional Mall Index (Bloomberg: FNMAL), had underperformed the benchmark year-to-date as of November 8 despite posting solid cash flow growth. The headline of brick-and-mortar retailers struggling to compete with e-commerce was the dominant theme, especially when coupled with department store closings.

Since the election, the shopping center and mall indexes are ahead of the benchmark by 120 bps each. We agree with the market in that the “Trump Effect” could stimulate more demand for retail space through enhanced retail sales and retailer profitability. Optimism surrounding the potential for comprehensive tax reform including lower income taxes has been the primary driver of the recent move. If personal and corporate taxes are lowered, we would expect increases in GDP, employment, and wages, which would help retail sales, the retailers, and finally retail real estate. President-elect Trump is also likely to put less upward pressure on the minimum wage, which could increase profit margins, particularly at brick-and-mortar locations, and thus driving the ability to pay higher rent.

Self Storage

2016 has been an extreme reversal in the recent trends for self storage performance as estimates for rental growth have reverted back to historical levels (see our September 2016 REIT Outlook). It was the worst performing sector prior to the election (underperforming the benchmark by almost 1600 bps!), and has also been the worst performing sector since the election. We believe this is unwarranted given that the sector has historically been able to grow in almost any environment as illustrated by the 4 D’s of demand: Death, Divorce, Downsizing, and Dislocation. In fact, LifeStorage (NYSE: LSI) has stated that the only time the company had negative rent growth was in 2009 when it reached -3%.

If anything, the demand picture for self storage is even more attractive since the election given that self storage has extremely short lease terms (second only to lodging), and thus would benefit quickly from any improvement in consumer confidence and spending. Inflation and high interest rates should also help to quell any exuberance on the part of private developers.

Triple Net

Historically, triple net REITs have had high correlations to interest rates, as their business of building diversified portfolios of long-duration single-tenant assets makes them more of a financing vehicle than a property owner/manager. Prior to the election, the interest rate decline produced outperformance versus the index of over 1500 bps and drove NAV premiums over 30%! The recent increase in interest rates has caused the sector to underperform by 410 bps since the election, eating into their significant NAV premiums. Going forward, lower stock prices, lower NAV premiums, and higher borrowing costs could dampen the sector’s ability to grow cash flow through acquisitions if acquisition yields don’t move up in tandem with their cost of capital. With little to no organic growth, these stocks will behave even more like bonds if rising interest rates and inflation continue to be a theme for the new administration.

Industrial

Prior to the election, the industrial sector was the top performer year-to-date, beating the index by over 2000 bps. While we maintain a positive outlook for industrial REIT fundamentals, we have slightly reduced our forward expectations for the sector since Trump was elected. His rhetoric regarding the renegotiation of the North American Free Trade Agreement (or NAFTA), China’s Most Favored Nation status, and blocking the passage of the Trans Pacific Partnership (or TPP) leads us to believe that foreign trade could decline, which would reduce port activity and thus real estate needs in such markets While industrial REIT exposure to the West Coast, Houston, and Miami is high, these markets are also partly driven by domestic activity such that the decline would likely be manageable.

This adjustment to our industrial outlook has to be put in the proper context, however. The available data on 2016 Black Friday and Cyber Monday indicates that online shopping will continue to drive a disproportionate share of retail sales growth, which gives us confidence that demand for e-commerce industrial real estate will remain strong regardless of US trade policies. The 70 bps of underperformance since the election seems appropriate given the added risks and uncertainty. Despite the slight pullback, the industrial sector continues to trade at high valuations relative to other sectors, leading us to believe that there is room for further declines in trade-related industrial real estate if any of Trump’s plans are enacted.

Data Centers and Cell Towers

Due to growth in the use of the cloud and mobile data, an equal-weighted index of data center and cell tower REITs was second only to industrial REITs in year-to-date total returns prior to the election. Our outlook for data center and cell tower REIT fundamentals has not changed, but the index has underperformed since November 8, mostly attributable to the cell towers. We believe that most of the negativity surrounds speculation that a Sprint (NYSE: S)/T-Mobile (NASDAQ: TMUS) merger would be possible under Trump, and secondly, the potential that the definition of ‘real estate’ is revisited under comprehensive tax reform such that the REIT status of this sector as well as some timber and billboard REITs could be in jeopardy.

While anything is possible, it seems unlikely that the REIT status would be repealed since the incremental revenue to the Treasury would be minimal (if not less!). Even if the S/TMUS merger were to be pursued and allowed, the 15%+ declines in the tower stock prices more than account for any loss of revenue on towers that have both S and TMUS sites. In fact, history shows that mergers with spectrum involved actually result in more leasing activity, not less.

Healthcare

Similar to triple net REITs, healthcare REITs have long term leases that cause the stocks to be among the most sensitive to changes in interest rates. While they benefited from low interest rates earlier in the year, the FTSE NAREIT Health Care Index (Bloomberg: FNHEA) performed merely inline with the benchmark. Since the election, the rise in interest rates and the prospect for a repeal of the Affordable Care Act (ACA, or Obamacare) has resulted in underperformance of 180 bps. A repeal or reform of the ACA would have negative implications for many tenants of the healthcare REITs. In particular, a decline in coverage would lead to fewer visits to both hospitals and medical office buildings. Though not associated with the ACA, skilled nursing facilities are funded mostly through Medicare and Medicaid, which could experience some disruption from a united Republican government.

Office

The FTSE NAREIT Office Index (Bloomberg: FNOFF) had a volatile year after a rough start, finishing about 70 bps ahead of the benchmark before the election. The sector has had the second best relative performance (+470 bps) since the election, mostly due to the potential for deregulation, which could allow the Financial sector to increase profits and hiring. This would have an outsized effect on Central Business District (or CBD) office companies that have had to rely on employment growth from Technology, Advertising, Media, and Information (or TAMI) tenants to lease the space that has been left by Financial companies. Secondary cities could also benefit if Trump’s trade policies bring back manufacturing and industrial jobs that had previously been lost due to cheaper labor abroad.

Alexandria (NYSE: ARE) in particular benefited from the Trump victory due to its high concentration of pharmaceutical tenants. Hillary Clinton’s criticism of these companies had strained ARE’s valuation on fears that this tenant group would be expanding less than they had under the previous administration. With Trump as the nominee, these negative expectations have been lifted, driving ARE’s +4.6% performance versus the RMZ at -0.6% since November 8.

Lodging

Last, but certainly not least, lodging has had the largest outperformance of all of the property types, totaling over 800 bps. The nature of a lodging lease being only 1 day makes it the most sensitive to the economy. As the country had been stuck in a low GDP growth environment for the past few years and with future GDP growth estimates coming down prior to the election, lodging had been a laggard for the prior two years, including trailing the benchmark by 80 bps as of November 8. Since the election, many GDP estimates have been raised as tax reform and other inflationary policies could have a positive effect on businesses and spending. Hotels will be the first properties to see the effects of any growth in jobs and corporate income, hopefully mitigating any negatives that may result from lower immigration and the strong dollar on international travel. To a lesser extent, any decrease in healthcare premiums for employers and employees could increase their ability to spend on travel for both leisure and business.

The Pro-America Portfolio

Given that 95% of all REIT net operating income comes from domestic properties, US REITs are an investment in the US economy. While we are sure each CEO has his or her own personal preferences for political leadership of the country, their companies are dependent upon the success (or lack thereof) of the country. We can’t be sure that the new administration will be able to deliver on all or even some of the promises that have been baked into the 3.6% increase in the S&P 500 from the election through November 25. However, we are confident that recent economic optimism and its impact on companies that are ultimately the tenants of REITs will have a positive impact on REIT fundamentals and sustain the current cycle that began in 2009.

Higher inflation via wage growth and cost of materials will only increase replacement cost, thereby driving up hurdles for new construction. Eventually, this will flow through REIT income statements via higher rents, enabling REITs to continue predictable increases in dividends. Our own analysis forecasts 5% annual dividend growth over the next three years for REITs in our portfolio. While there may be some short-term disruption in REIT prices while they attempt to find an equilibrium in a new interest rate environment, we believe the above average dividend yield spread and NAV discount of 10% as of November 25 more than discounts any risk associated with rising interest rates.

Parker Rhea, prhea@chiltonreit.com, (713) 243-3211

Matthew R. Werner, CFA, mwerner@chiltonreit.com, (713) 243-3234

Bruce G. Garrison, CFA, bgarrison@chiltonreit.com, (713) 243-3233

Blane T. Cheatham, bcheatham@chiltonreit.com, (713) 243-3266

RMS: 1904 (1.31.2017) vs. 1904 (12.31.2016) vs. 346 (3.6.2009) and 1330 (2.7.2007)

Previous editions of the Chilton Capital REIT Outlook are available at www.chiltonreit.com/reit-outlook.html.

An investment cannot be made directly in an index. The funds consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.

The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security.

for more info on our strategy

go now →

for more info on our strategy

go now →

VIEW CHILTON'S LATEST

Media Features

go now →

Contact Us

READ THE LATEST

REIT Outlook

go now →