Equity REITs: Takeaways from REITWeek 2026 | July 2026

We recently attended the annual REITWeek conference in New York City, where we conducted 39 management meetings, toured several properties, attended peer dinners, and caught the infectious energy of the Knicks taking Game 1 of the NBA Finals.

The tone was more constructive than in recent years, especially considering a fairly noisy backdrop. The 10-year Treasury had backed up to ~4.4%, inflation concerns remain despite a potential Middle East resolution, and midterm elections are approaching, which can draw investors’ attention away from stocks and related fundamentals. None of it seemed to be damping business plans for high-quality REITs.

A few themes cut across most property types. The most omnipresent was artificial intelligence, which surfaced in nearly every meeting and was consistently framed as a net positive for REITs. However, for our team, the most important story is the outlook for accelerating earnings growth. Most importantly, management teams recognize earnings growth is increasingly taking importance from traditional REIT metrics as generalist investors represent the marginal buyer more than ever for REITs.

Most importantly, and underpinning our bullish stance on REITs, earnings growth is accelerating to the 6-7% range in the coming years compared to the long term average of ~3-4%, and, we think this period of above normal growth extends until rents rise enough to justify meaningful new construction (several years for most property types). Similar to last year, we left the conference with a handful of actionable takeaways, and more confident in strengthening the fundamental outlook across most sectors.

Shopping Centers

Our team met with InvenTrust Properties (NYSE: IVT), Brixmor (NYSE: BRX), CTO Realty (NYSE: CTO), Curbline Properties (NYSE: CURB), Federal Properties (NYSE: FRT), Kite Realty Group (NYSE: KRG), Regency Centers (NYSE: REG), and Tanger (NYSE: SKT)

On the robust transaction market, the private market appetite has defied rising interest rates both from a volume and cap rate perspective. Importantly, the REIT benefit is currently double sided, with the ability to recycle out of mature slower growth centers at good prices and still find faster growing targets in an often immediately accretive manner.

On the leasing front we heard reports of one of the most upbeat ICSC (International Council of Shopping Centers) conventions in years. While brokers are known to be upbeat, the salient takeaways for tenant behavior were 1) major retailers engaging on space needs earlier than ever (2029+), and 2) tenants are more flexible on the spaces they are willing to rent. Both points reflect the increasingly limited availability of quality retail space. Even though fundamentals are robust, ground up development (in most cases) requires ~20% higher rents to earn justifiable returns. The exception has been REG, where relationship-driven grocer anchored development still makes sense, though it remains a small investment relative to its capital base. For most of the REITs, targeted redevelopment and acquisitions are the best uses of capital today. Overall, we left NAREIT even more positive on this group. The potential combination of accelerating growth and multiple expansion is palpable. We remain overweight this group and continue to monitor for additional entry points/opportunities.

Healthcare

The hallway chatter was nearly as intriguing as the management meetings this year for healthcare REITs. Senior Housing REITs released solid mid-quarter operating updates at the start of the conference, but market volatility brought a material pullback across the group (between May 26th and June 3rd: WELL -9%, VTR -11%, AHR -9%, and SBRA -13%). Theories included generalist rotation and abnormal flows ahead of large IPOs, but our channel checks revealed no deterioration in fundamentals. Consequently, we took the volatility as an opportunity to increase exposure to this attractive group, which has thus far proved timely as most of the names have regained late May price levels. Please read our December 2025 SH Outlook for more on our bullish stance.

Outside of SH, we had the opportunity to meet with our Medical Outpatient (MOB) positions, Healthcare Realty (NYSE: HR) and Healthpeak Properties (NYSE: DOC). In line with recent conversations, MOB private market interest is increasing amid a backdrop of ratable but accelerating earnings growth. In life science, we heard optimism around emerging green shoots, though we remain cautious on the timing lag for leasing success to translate into actual earnings growth.

Healthcare remains one of our largest overweights, and nothing at the conference lessened our conviction. We are most positive on senior housing, where the multi-year supply/demand setup remains the most compelling in the REIT universe. Our decision to add during the late-May pullback reflects how attractive we find the group at current levels. On the MOB side, our continued enthusiasm is being validated by strong year-to-date total returns (DOC/HR +38%/+22% through June 30th), with the deepening private market interest finally being reflected in the public markets.

Data Centers

We met with Digital Realty Trust (NYSE: DLR) and Equinix (NASDAQ: EQIX). With seemingly insatiable demand, data center REITs have become increasingly picky on tenant signing and timing. For example, the newly extended leasing window (tenants willing to lease space up to 24 months before delivery) doesn’t necessitate that landlords actually lease the space as rents will likely be higher 12-24 months out. In addition, ‘Neoclouds’ are growing aggressively and would like to take space in DLR and EQIX new developments. Neocloud providers, which include CoreWeave (NASDAQ: CRWV) and Nebius (NASDAQ: NBIS), rent out GPU chip capacity to AI users, attempting to capture a spread. However, DLR and EQIX have not engaged with these companies given poor credit, low capacity to pay rent, and pre-existing relationships with the customers of Neoclouds.

Outside of power availability, the biggest hindrance to new supply is NIMBY-ism (Not in My Backyard). According to REIT management teams, the anti-development campaigns are largely funded by international groups that would like to slow our country’s lead in AI. The primary complaints of these groups are that new data centers will: 1) increase electricity costs; 2) deplete water resources; 3) create fewer jobs than a traditional commercial building; and 4) contribute to a future where AI takes away jobs. While the data behind these claims are uncertain at best, the movement has been successful in prolonging approval processes and has even resulted in several municipalities nationwide restricting any future data center development.

From a landlord perspective, the restriction of future supply should only increase rents and organic growth for stabilized data centers, or those that have already been approved. However, the future development pipelines for DLR and EQIX could be at risk if the drumbeat continues to grow louder and results in less activity. At Chilton, we ascribe little value to unapproved development projects to mitigate this risk.

Office

Ahead of the conference, we toured the sales gallery for 343 Madison Ave. in New York City and rode the site’s recently opened Grand Central entrance at 45th and Madison into the LIRR concourse (highlighting the project’s long term obsolescence immunity). During the tour, BXP noted that the previously signed tenant (Starr Insurance) exercised its option for two additional floors, and, shortly after the conference, McDermott Will & Schulte signed a lease for 150,000 square feet (floors 31-37), bringing the project to 56% pre-leased. This pre-leasing level (plus the top floor bank remaining available at elevated rents) should command attractive terms from equity partners, which will lessen the capital burden on BXP while increasing returns.

We met with the management teams of BXP Properties (NYSE: BXP), Highwoods Properties (NYSE: HIW), Cousins Properties (NYSE: CUZ), COPT Defense Properties (NYSE: CDP), Kilroy Realty (NYSE: KRC) and Piedmont Realty (NYSE: PDM). Similar to messaging in recent quarters, the runway from pent-up return-to-work demand is longer than the draconian scenarios implied and remains a major driver of improved leasing despite a softer job market. However, the bigger story was AI-related leasing, which has not only been firing up San Francisco’s market, but is spreading to other regions (notably NYC). Beyond popular AI names taking office space (e.g. Anthropic, OpenAI), we heard more about companies building internal AI platforms (law firm Kirkland & Ellis’ $500 million investment announcement was a notable example), again rebuking the March narrative that AI would destroy traditional industries such as law firms. While AI’s long term demand impact is hard to quantify at this juncture, leasing statistics show that office users are putting long term money into space for their employees.

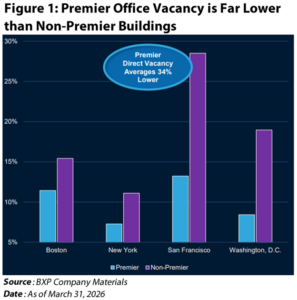

The other important driver for Office REITs is the continual widening of the market’s quality bifurcation. As one landlord put it, every tenant in an A- building is now a target, and the upside in high quality buildings has room to run as long as any occupancy remains in A- buildings. Figure 1 shows how this is already reflected in today’s market (premier vacancy is ~34% lower relative to non-premier), and we expect this gap to widen.

We remain positive on office and are overweight through BXP (gateway) and CUZ (Sun Belt). The SF ramp has us looking harder at the West Coast, but we like our major market exposure through BXP and the increasing demand in the Sunbelt, particularly Dallas and Charlotte, that is benefiting CUZ.

Self-Storage

We met with Extra Space Storage (NYSE: EXR), CubeSmart (NYSE: CUBE), and SmartStop Self Storage (NYSE: SMA). In our March 2026 REIT Outlook, we asked when the sector would finally inflect; the answer at NAREIT was that it’s starting to…but slowly. Occupancy gaps to last year have largely closed (EXR ended May flat y/y at 94.2%, after running down 40 bps in the first quarter) and move-in rates turned slightly positive for a few operators following a long stretch in the red. Churn is falling, with Public Storage (NYSE: PSA) running ~300 basis points (bps) better than a year ago. Management teams also described seasonality that looked ’normal’ for the first time in years. However, with housing mobility still subdued, the improvement reads more as a function of falling supply (Figure 2) and easing comps rather than a genuine recovery in demand. One clear positive, Los Angeles recently lifted the pricing restrictions tied to the January 2025 wildfires, removing a revenue headwind.

SMA remains one of the more interesting stories in the sector. In-place rents are still climbing, with existing customer rent increases (ECRIs) in the mid-20% range, helping keep same-store revenue growth positive for six straight quarters. Move-in rates were down ~5% y/y in May, but that’s against the toughest comp in the group, as SMA was the only storage REIT to post positive same-store NOI growth last year. A few of the more notable earnings growth drivers, though, sit outside the core portfolio. SMA’s bridge lending platform targets low-to-mid teens returns and feeds a captive acquisition pipeline, while its ~$1.1 billion managed-REIT platform adds a steady stream of fee income. Argus, SMA’s recently acquired third-party management business presents an opportunity to scale and improve margins. With the stock trading near a ~19% discount to NAV while peers sit much closer to parity, we think the setup skews to the upside from here.

Triple Net

We met with Realty Income (NYSE: O), Getty Realty (NYSE: GTY), NNN REIT (NYSE: NNN), and FrontView REIT (NYSE: FVR). We came away positive on the group as tenant credit is strong and external growth is accelerating, two themes we highlighted in our November 2025 REIT Outlook. First, the blended cost of capital is still allowing for accretive acquisitions. Secondly, NNN was a clean example on improving credit since it took just 11 bps of bad debt in the first quarter against a 75-bps full-year assumption, the main driver of its recent guidance raise. Furthermore, it renewed 36 of 43 expiring leases at ~2% above the prior rent. NNN remains the disciplined compounder of the group, but it is trending toward the high end of its acquisition guidance and carries the longest debt maturity ladder in the sector at over 10 years.

GTY was one of our more constructive meetings as management presented a clean illustration of the spread math driving improved results. GTY’s 26% year-to-date total return has pulled their cost of equity lower, bringing the all-in cost of capital to the mid-6s against acquisition cap rates in the high 7s. That ~100-150 bps spread, paired with a sizable pipeline that’s ~90% relationship-sourced rather than brokered, should comfortably support +4-5% earnings growth moving forward based upon our analysis. Combined with a dividend yield of 5.8%, GTY presents an attractive total return story.

FVR, has been our top performer with the net lease sector with a 40% total return year-to-date. It recently raised 2026 AFFO guidance to 5% growth at the midpoint, its third straight increase, and took zero bad debt in the first quarter. The company has been successful in recycling tenants in multiple industries. For example, a former Walgreens was re-leased to Amazon at the same rent, and a batch of tertiary-market Dollar Trees were sold to institutional buyers and recycled into stronger real estate. Leverage sits at a comfortable 5.3x net debt/EBITDA and the company is positioned to see a Fitch rating in the not too distant future, as well.

Industrial

Within the traditional industrial space, we met with EastGroup (NYSE: EGP) and Terreno (NYSE: TRNO). The operating environment remains solid with signs of further improvement in many markets. Indeed, after a period of heavy supply deliveries in recent years, absorption and rents are now improving across most of the country, with pockets of exceptional strength (South Florida, DFW/Houston, the NYC boroughs). The only lagging markets today include SoCal and Seattle, but even for those two pressured regions, we are seeing specific submarkets firming (advanced manufacturing demand in LA’s Manhattan Beach/El Segundo submarkets has been exceptional). The magnitude of data center related leasing (e.g. firms that are participating in the buildout of data centers) continued to impress, with PLD citing 10% of total leasing driven by data center construction. We think this tailwind is bigger than appreciated and we remain modestly overweight the sector.

Outside of traditional industrial, we also met with both cold storage REITs – Americold (NYSE: COLD) and Lineage (NYSE: LINE). COLD’s recently announced JV was the headline news as investors prodded for more portfolio and valuation specifics. On the fundamental side, both management teams suggested the market was entering a more normalized period for volumes after a long period of lackluster activity. We remain cautious on the group and thus maintain no exposure to cold storage.

Multifamily

We met with Mid-America Apartments (NYSE: MAA), Camden Property Trust (NYSE: CPT), Independence Realty Trust (NYSE: IRT), and Centerspace (NYSE: CSR). The two largest names in the sector, AvalonBay (NYSE: AVB) and Equity Residential (NYSE: EQR), skipped the conference given their pending merger that will create one of the largest REITs with a market capitalization of over $50 billion.

The clearest message of the week was that new lease rate growth is showing signs of positive inflection, which has not been seen nationwide since late 2021. For reference, MAA’s new lease pricing improved 210 bps from 1Q26 to May, now at -4.9%, which, combined with +5.4% renewals, blends to +1.1% on mid-95% occupancy. However, this is the same ’next year’ Sun Belt narrative we’ve heard for several conferences running, so, not surprisingly, many investors seem to be in ‘wait and see’ mode. However, the underperformance by apartments year to date has made the risk versus reward look more attractive.

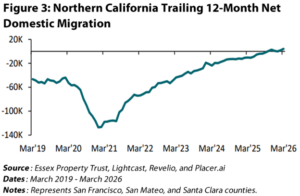

The Bay Area is a notable bright spot, where new-lease rates increased 15-20% in May for some operators, driven by a surge in AI-related job growth (postings jumped from ~3,000 in 2023 to ~11,000 through the first five months of 2026). Impressively, the region’s net domestic migration turned positive for the first time in several years (Figure 3).

Centerspace, meanwhile, opened NAREIT by wrapping up its strategic review after seven long months with disappointing news. The result: only ~$245 million of asset sales under contract (exiting Rapid City, Bismarck, and one Denver asset), pulling leverage from 8.2x net debt/EBITDA down into the high 6s and funding a special dividend rather than a full sale of the company. Frictional costs, thin bid depth, and a rising buyer cost of capital sank the larger deal, according to management. Following the announcement, we exited our position entirely. Overall, we remain slightly underweight multifamily due to muted rent growth while peak supply is being digested, balanced by attractive valuations against a backdrop for the eventual inflection of rent growth.

Single Family Rentals (SFR)

We met with Invitation Homes (NYSE: INVH) and American Homes 4 Rent (NYSE: AMH), two of the largest owners in the space with ~170,000 homes combined. Fundamentals remain solid, supported by stable occupancy (~97%) and renewals carrying a floor in the low-to-mid 3% range, while new lease spreads have flipped positive, a clear contrast with apartments. Bad debt sits near record lows and resident income growth still outpaces rents. With millennials (35-49 years old) aging into prime years for single-family living, SFR’s offer a compelling option in an environment where home ownership is out of reach for many households.

The bigger story for the group, however, remains the 21st Century ROAD to Housing Act. What began as a January 2026 Truth Social post from President Trump, pledging to “ban institutional investors from buying more single-family homes,” froze external growth and left investors unwilling to underwrite the names through months of uncertainty. A final compromise, built on the House framework that spared build-to-rent and killed the Senate’s seven-year forced-sale provision on Built-to-Rent development, has passed the House and Senate, awaiting President’s signature. President Trump has since refused to sign the bill unless Congress takes up his SAVE Act, which aims to improve voter integrity. Whether it ultimately is signed into law or not, one thing is clear: institutional SFR owners remain in the crosshairs of politicians in both parties. Both names trade at a meaningful discount to NAV, but with no near-term catalyst to close the gap. We are underweight the sector as neither an inflection in earnings growth nor a change in political rhetoric appear to be in the cards in the near-term.

Manufactured Housing / RVs

We met with Sun Communities (NYSE: SUI) and Equity LifeStyle Properties (NYSE: ELS), both focused on manufactured housing (MH) and RV parks. Recall, SUI has meaningfully reshaped its portfolio over the last several years, with the Safe Harbor marina sale in 2025, followed by the UK Park Holidays exit in late May. The latest sales leaves ~$1.0 billion of proceeds to put to work, likely split between share buybacks and MH acquisitions at low-to-mid 4% cap rates.

The MH business is tracking in line with guidance for both ELS and SUI, which call for 5.5-6.5% same store NOI growth, well above all other residential REITs. With high quality acquisitions tough to come by, both are concentrating on building out sites on existing land, which carries a yield in the high single digit range. RV’s, which account for 30% of SUI NOI, are experiencing a normalization of the transient business after several years of underperformance (now tracking slightly ahead of guidance). We remain slightly overweight the sector through SUI, where a cleaner, more focused business model under the leadership of a new CEO should drive a higher re-rating over time.

Cell Towers

We met with American Tower (NYSE: AMT), the largest cell tower REIT and an owner of a prominent data center company (CoreSite). Starting with cell towers, the company is still confident that 4.5% long term organic revenue growth from towers is possible given high single digit growth in the international business and about 4% domestically. Mobile traffic per smartphone is projected to more than double from 2025-2030, supporting these assumptions. These targets do not include any upside from AI, which has yet to drive new investment by carriers in towers. Currently, most sites on towers do not have the capacity for the amount of uplink data that is needed to perform AI tasks. Any upgrades by the carriers to support this activity would increase organic revenue growth assumptions. In addition, the 6G upgrade cycle is now 4-5 years away, which should result in considerable activity from the carriers.

The approval for Starlink to acquire spectrum from DISH, as well as the recent IPO of SpaceX (NYSE: SPCX) is not viewed as a risk to terrestrial carriers such as AT&T, T-Mobile, and Verizon. In fact, AMT sees potential for any traction that Starlink makes in becoming a carrier will only increase investment in towers by the terrestrial carriers. The company has already assumed no future payments from DISH after it defaulted on its obligations late last year, though AMT is optimistic it will recover its share of the $2.4 billion put in escrow for the lawsuits, plus there is potential for recoveries beyond what is currently in escrow.

Management believes that it is not getting credit for its data centers inside of AMT and conceded that it is open to exploring options to maximize the value for shareholders. While they did not hint at any specific transactions, we believe a sale, spin-off, or re-IPO could be a catalyst for the stock. Despite the incredible economics of data center development (yields in the mid-teens), AMT still believes the best business model in the world is the cell tower business.

Conclusion

While uncertainty hasn’t disappeared, we believe the REITs are entering a period of above average earnings growth that, in our view, remains underappreciated in today’s market. Indeed, as we touched on above, earnings growth is accelerating across most property types. Most importantly, given the current state of construction and financing costs, we believe REIT growth has an impressive runway until rents reach levels that justify new development.

Matthew R. Werner, CFA

mwerner@chiltoncapital.com

(713) 243- 3234

Bruce G. Garrison, CFA

bgarrison@chiltoncapital.com

(713) 243-3233

Thomas P. Murphy, CFA

tmurphy@chiltoncapital.com

(713) 243-3211

Isaac A. Shrand, CFA

ishrand@chiltoncapital.com

(713) 243-3219

VNQ: $96.39 (6.30.2026) vs. $88.49 (12.31.2025) vs. $116.01 (12.31.2021) vs. $56.91 (3.23.2020)

An investment cannot be made directly in an index. The funds consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.)

The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward-looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security. Past performance does not guarantee future results.

Information contained herein is derived from and based upon data licensed from one or more unaffiliated third parties, such as Bloomberg L.P. The data contained herein is not guaranteed as to its accuracy or completeness and no warranties are made with respect to results obtained from its use. While every effort is made to provide reports free from errors, they are derived from data received from one or more third parties and, as a result, complete accuracy cannot be guaranteed.

Index and ETF performances [RMZ, VNQ, and FNER] are presented as a benchmark for reference only and does not imply any portfolio will achieve similar returns, volatility or any characteristics similar to any actual portfolio. The composition of a benchmark index may not reflect the manner in which any is constructed in relation to expected or achieved returns, investment holdings, sectors, correlations, concentrations or tracking error targets, all of which are subject to change over time.

Leave a Reply

for more info on our strategy

go now →

for more info on our strategy

go now →

VIEW CHILTON'S LATEST

Media Features

go now →

Contact Us

READ THE LATEST

REIT Outlook

go now →